You may be a full-fledged Fintech app like PayPal or a media streaming app like Netflix that asks users to pay for subscriptions in-app, it is important to note that there is one thing that you can't afford to miss- PCI DSS Compliance.

Failure to examine effectively the PCI safety standards that leads to a data breach can actually lead to devastating financial consequences such as fees, fines, and even business losses.

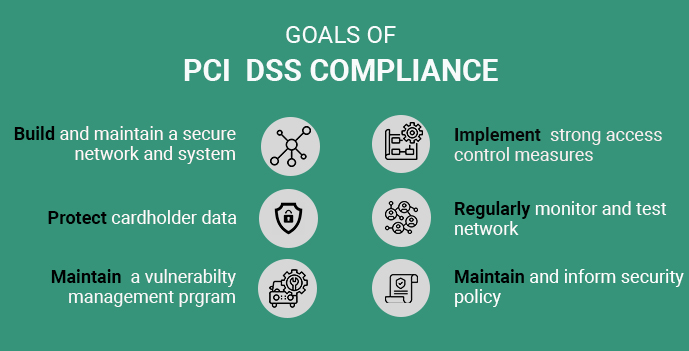

The PCI Payment Card Industry Data Security Standard (PCI DSS) is a highly prescriptive technical standard aimed at protecting credit and debit card details, which is normally known as cardholder data" in the industry.

The purpose of PCI DSS is to save payment card fraud by securing the data of cardholders within those organizations that accept card payments. Compliance with PCI is mostly based around IT infrastructure.

Maximum PCI DSS requirements affecting the Fintech app development process are covered by Requirements 3, 4 and 6. Let's look at all three of them separately to get a full understanding of the recommendations for the PCI range.

Data from the cardholder denotes information that is processed, printed, stored or transmitted on the payment card. The applications that accept payment by card are supposed to protect the data of cardholders and prevent unauthorized use, regardless of whether the data is printed on the card or stored locally.

Generally, no data from cardholders should be stored until it is absolutely necessary for business needs to be met. The sensitive data mentioned on the magnetic stripe should never be stored and should be rendered unreadable in case you need to store the PAN details.

Hackers are not especially unable to intercept the transmission of cardholders ' information through free, public networks, and shielding private data from them is very necessary. One way to do this is through data encryption.

Strong security protocols and encryption such as TLS / SSL and IPSec or SSH should be used by app development companies to safeguard the sensitive data of cardholders during their public network transmission. End-user messaging systems should never submit insecure PANs

This provision of PCI compliance is in terms of developing external and internal applications that are deemed to be within the scope of PCI DSS enforcement. This is the case for any developed app that collects, stores and transmits the information of the cardholders.

The PCI payment applications created by the Fintech App Development Companies to be used by external organizations should conform to the Payment Application Data Security Standard (PA-DSS) and should be evaluated by PA-QSA.

Compliance with the requirement requires a properly documented register of libraries and tools software assets that are used in the development cycle of software. Each item in the software asset register should include a version number How and where software is used Clear explanation of their function.

Because the software libraries and tools are frequently updated, it is of paramount importance that the register is continuously reviewed and kept up to date. Once a software asset register has been established, a process should be implemented to monitor each item in the register for sending vulnerability notification and updated releases on a regular basis.

The PCI DSS compliance phases can be divided into two parts: the first part is to achieve a PCI DSS compliance status- which can be made by creating a PCI compliance checklist- and the second part is to maintain a PCI DSS compliance status.

The second part- remaining compliant in PCI DSS is a difficult state to achieve, often due to misconceptions that compliance is simply about following the PCI DSS audit checklist. The formula to maintain compliance is to develop processes that deliver a state that continues to comply with PCI.

Holding detailed records of security procedures and enforcing supervision by management is a critical approach to holding complacency from entering the system and ensuring that a state of compliance with PCI DSS can be checked at any time.

Software developer and solution provider with over 7 years of experience, including general management of mid to large size organizations, corporate development, product development, business operations, and strategies. Currently managers at EPixelSoft- A Software Development Company- A one-stop-sho... View more...